A Peak into 2024

A Peak into 2024

What this year has in store for us #40

Welcome to the first edition of 2024! After two good weeks of vacation from Notes by Letícia, we are back with biweekly content delivered to your email every Wednesday morning. As I mentioned in the last edition, one of the things that writing maximizes is serendipity, so this edition, and the upcoming ones, will be in English.

You may have read the title and thought, 'another prediction,' yes, another prediction. However, my goal here is not to expect everything I write to happen, but rather, an exercise in reflecting on what might happen and why it would or wouldn't happen.

If you want to receive the Notes by Letícia in your email every Wednesday, biweekly, subscribe now!

A prediction covers various sectors and distinct markets, so I'll comment on some points that have indicators of change. Let's go through some topics, ranging from fundraising for startups, fundraising for investors, liquidity, and specific sectors.

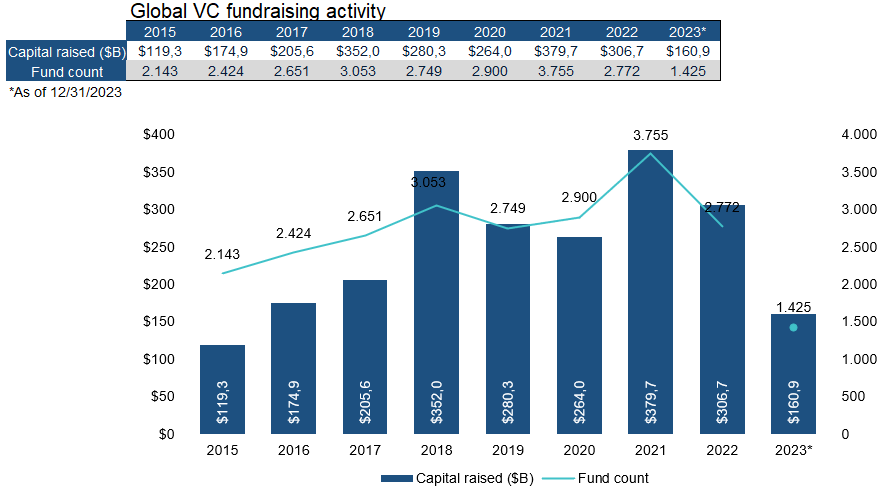

Fundraising for VCs

2023 was different from the past years, the amount raised is in line with the numbers from 2016 and 2017, far from what was seen in the last 2 years. Additionally, the number of funds have also decreased significantly, indicating a trend of reducing fund sizes and/or a greater concentration of investments in funds with a well-known reputation in the market.

In 2023, we saw major funds lowering their fundraising targets, such as Tiger Global, while other funds, like Kaszek, concluded the fundraising for two new funds, totaling almost USD 1 billion.

As public market conditions and interest rates were not in an ideal scenario for higher-risk investments globally, many investors chose not to increase their exposure to this asset class. In addition to the less favorable conditions, there was a lower activity in investment exits, which is the moment when investors receive their gains and capital back.

However, this public scenario is already changing in favor of higher-risk investments. Nevertheless, due to the long-term nature of investments in this asset class, the effects may take time to reach the private market and alter the observed numbers.

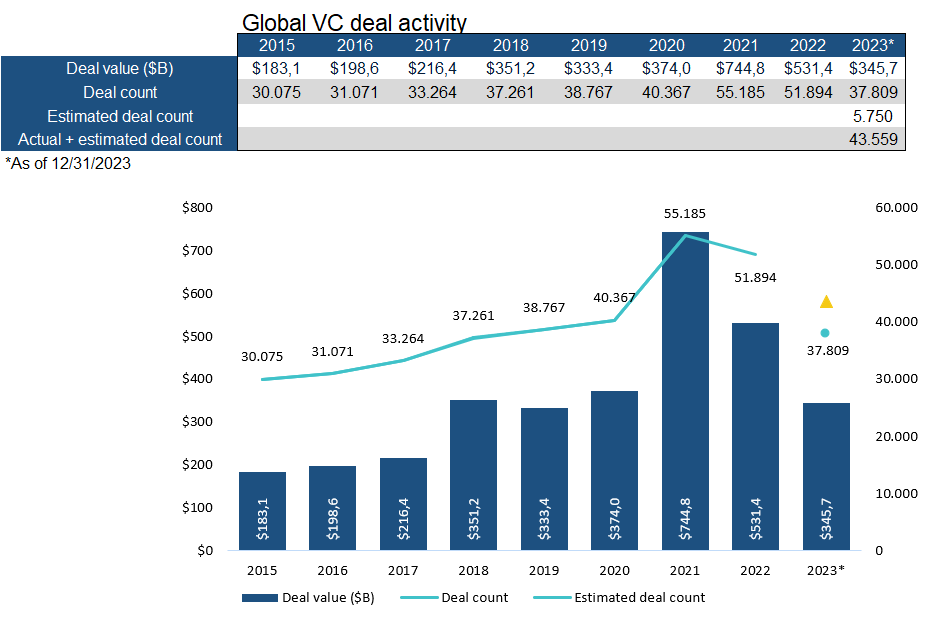

Fundraising for startups

The year 2023 was challenging for many startups, and I don't see signs of a significant improvement. The key indicator here is the amount invested, which falls between the levels seen in 2019 and 2020. However, as the saying goes, this doesn't mean that promising startups will be left without funding. Though, startups with more complex models to achieve market fit and those lacking a healthy business model will face greater difficulties in securing funding.

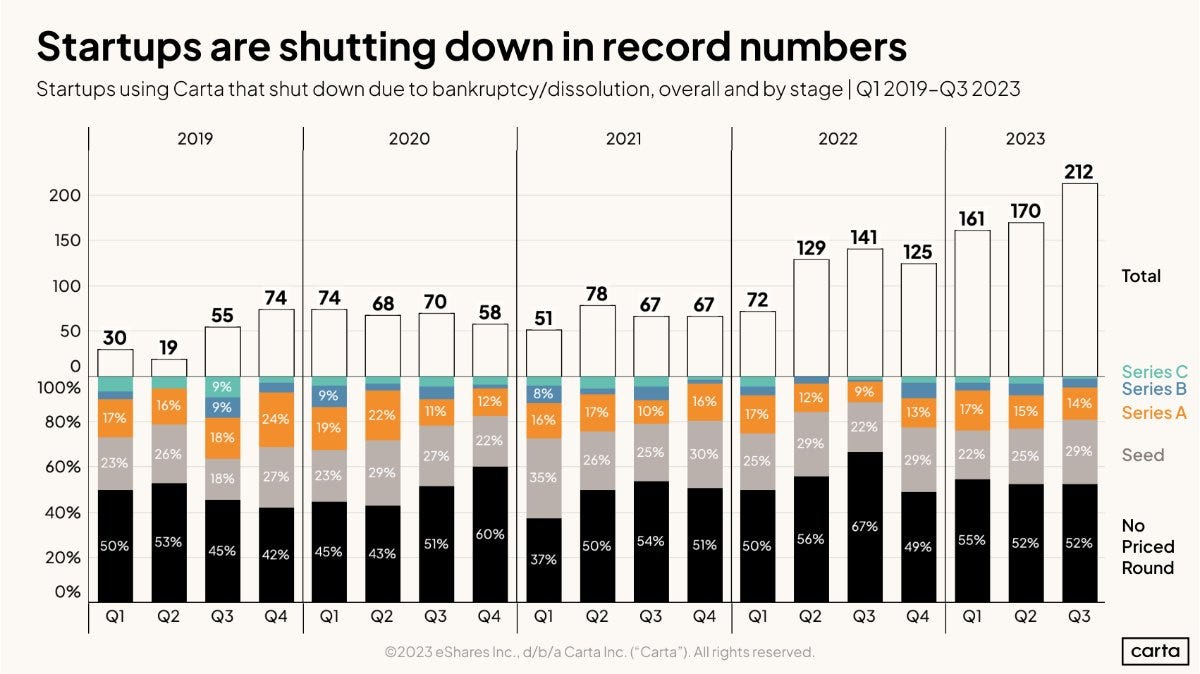

Another indicator of the fundraising challenges in 2023 was the number of startups that ended up being written off from various portfolios as they closed down. The chart from Carta clearly illustrates the difference in the number of startups that closed in 2022 and 2023 compared to previous years, and this trend is expected to continue in 2024. I believe that due to the rapid growth of the Venture Capital category in the past 3 years, the effects will still be visible for some years to come, due to to internal rounds and layoffs that extended the runway for some startups and only now are in need of cash.

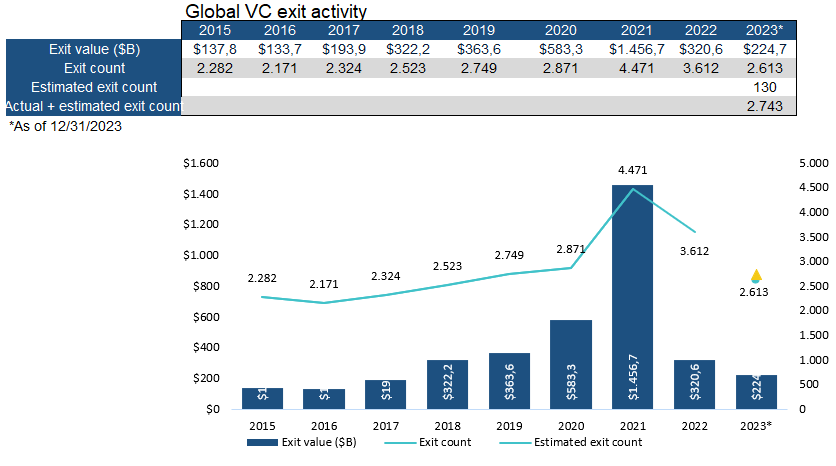

Liquidity

As mentioned above, this topic is intrinsically connected to VC fundraising, which consequently conects with startup fundraising. The moment of liquidity is crucial, as it is the most significant time for LPs and the Venture Capital business. It's when the money returns, with a premium, without this, the business model wouldn't sustain itself.

The number of exits observed in 2023 aligned with the levels seen in 2020. A reflection here is, what is the norm? Could it be that the last few years deviated from the norm, and we are now returning to the regular market pace? We encountered a hurdle that slowed down the market speed, but I believe it should gradually return and grow until the end of 2024. We have already seen some VC-backed startups going public in 2023, such as Klaviyo and Instacart. Hence, I anticipate more startups taking this path, but likely only those with performance comparable to what the public market expects. Last year, I discussed a bit about liquidity activity, especially IPOs, and the number of startups in line for this path of liquidity, click here to take a look.

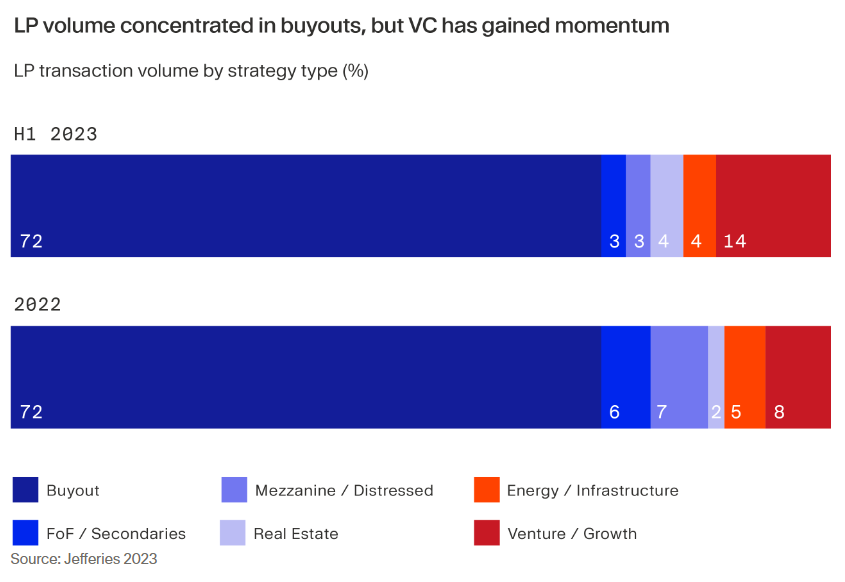

When I refer to liquidity in VC, I don't mean only IPOs and acquisitions but also the secondary market, which has a significant impact on investor liquidity. Many VCs sought secondary exits for their portfolio stake, with one of the main objectives being to deliver results for their LPs.

The so-called denominator effect has also contributed to the heightened secondary activity among LPs. It occurs when prices of public equities and bonds decrease but, since private alternatives adjust to market conditions with a months-long delay, investors' portfolios may suddenly become over-allocated to private markets. To correct this imbalance that institutional investors, in particular, have faced during the past 18 months, LPs frequently have turned to secondary markets to exit selected positions. - Moonfare Insights

AI

Yes, once again, the topic of AI is being mentioned in a newsletter as a prediction for 2024. Within the AI stack, last year saw a significant focus on foundation models, which are the ones that build and train models. Some of the key players in this sector include OpenAI, Anthropic, Bard, Grok, Llama, and Inflection. I believe that the winners in this sector, as well as new entrants, will require substantial funding, a wealth of data, and users (individuals and/or corporations). In 2024, we will likely see the emergence of clear leaders and the continued presence of others. However, I don't anticipate a large number of new entrants.

With a growing base of players developing artificial intelligence models, there is a market for applications built on top of these models. This ranges from SaaS platforms becoming increasingly AI-driven to the verticalization of solutions created on top of Large Language Models (LLMs). An intriguing development that I'm curious to see unfold is the GPT Store, where you can tailor GPT to your specific problem. This has the potential to bring an interesting dynamic to the market. I wrote about this last year, and you can click here to read more.

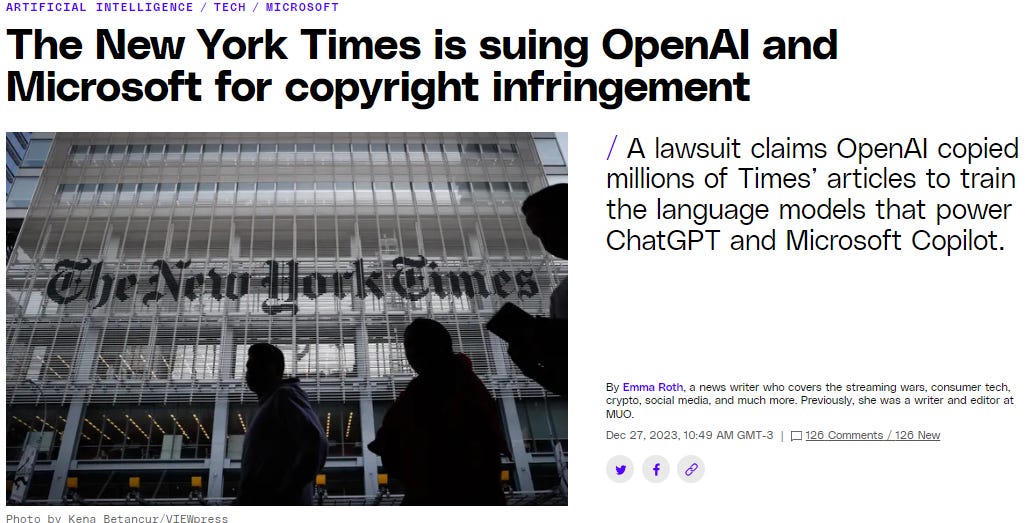

2024 will also be the year of disputes over what belongs to whom and whether something belongs to someone. This year will mark the beginning of discussions and the search for a solution regarding the training of a Large Language Model (LLM). It starts with The New York Times suing OpenAI for the use of content generated by the newspaper. Model training is based on data, and the more, the better. However, the question arises: should the owner of the content be compensated due to intellectual property considerations?

The model needs to understand patterns, and the most effective way to achieve that is by building on what humanity has already produced. However, the output shouldn't be a direct copy or use specific content. Hence, the question arises of how to navigate this new scenario. Benedict Evans shares his insights on this matter in this link, and it's worth a read.

Also related to AI, another significant topic that I believe we will see further development in is the multimodal capability of AI. Beyond producing text as an output, it is already possible to generate images, videos, and audio from text, as well as accept inputs that are not just text but also include images, videos, and voice.

Meta has disclosed tests on its glasses using multimodal AI to bring real-world interactions, with inputs being images and sounds happening in real-time.

I believe this functionality will linger in the limbo between being a real and practical use case, where there will be some possible applications, but only early adopters will have this experience initially.

Other Sectors

Crypto & Web3

Especially in Brazil, it will be an area widely explored by the activity of digital real (Drex), with global regulation being defined. The infrastructure here that will enable new financial players to enter this market will be very important.

Climate

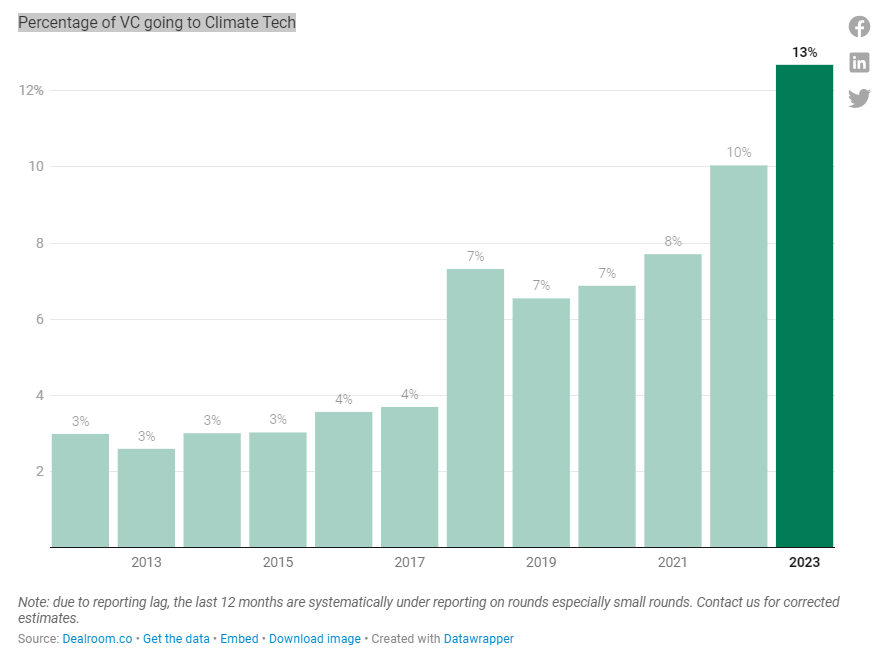

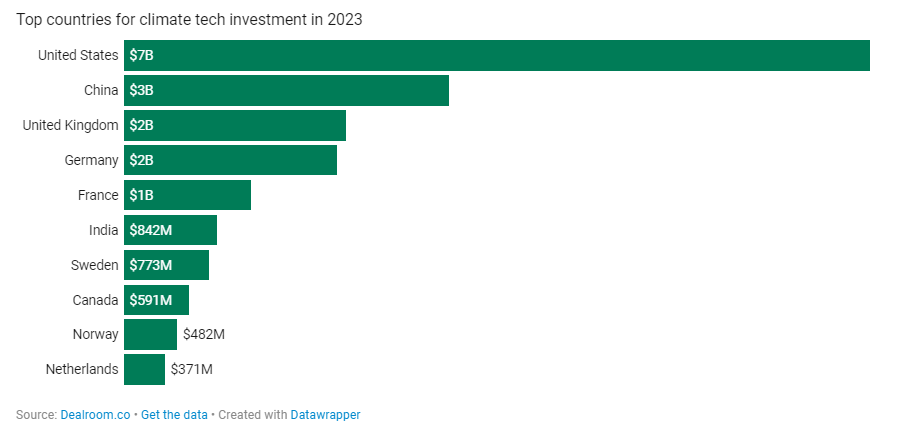

Not yet significant in Brazil, but it's a sector that has been growing in investment volume over the years. In 2023, Climate Techs' VC activity represented approximately 13%, showing an increase since 2019.

I recommend reading this report on Climate VC Activity in 2023 if you want to understand more about the topic. Regarding this sector, I only see growth, given the rise of new technologies such as AI and the urgency of the topic, driving the development of solutions for significant challenges.

As I mentioned at the beginning, the goal here is not to accurately predict everything that will happen but rather to observe some indicators from 2023 that may point to events in 2024. I believe this year will still be challenging, but with less anticipation in the fundraising market, following the trend observed in 2023 with fewer movements. I am excited about how the AI market will evolve and how it will impact other sectors.

Thank you for your support in this newsletter, and here's to another year!

Before reading the reccomendations don’t forget to subscribe!

Recommendations

⬛ Product-led growth’s failure - Product Hunt

⬛ Predictions 2024 curated and published by Rohit Yadav, CAIA

⬛ The red flags and magic numbers that investors look for in your startup’s metrics - Andrew Chen

First at all: Happy New Year! This note was really insightful and put me to think about many things that we saw at the private market last year. For 2024, my bet is similar to yours, with the top sectors definitely being AI and sustainability. The agenda of many companies are related with this concerns and technologies. In addition, there are really good startups, with solid thesis and rational cash position and projections. Let's share and learning together!