2024 YTD Highlights

2024 YTD Highlights

How 2024 has been so far... #52

Welcome to Notes by Letícia, a biweekly newsletter, in which I share my perspective on the Venture Capital market. My objective is to share my thoughts and bring up rich discussions about this ecosystem, from why it is how it is, to deep dive into some sectors.

If you’re curious about this market as well subscribe to this newsletter, and join the +740 people who receive an article biweekly.

In the blink of an eye we are already in August, it’s amazing how time flies. At the start of the year everybody was eager to understand what would be the year’s hypes, downfalls, and highlights (I also wrote a “prediction” then, if you want to check it out). Now, just past the halfway mark of the year, I thought it would be great to take a look back at how the year has been going, the doubts that still remain, and what to expect.

Starting the year the expectation around Brazil’s Selic was to drop to one digit, however, until this moment there is no indication that this is happening. This affects the risk-taking appetite for all investors, since it’s better to have a little lower return sometimes with almost no risk, than having a sightly higher return, but with much higher risk. The scenario is not that different in the United States, since it is experiencing one of the highest rates in a long time.

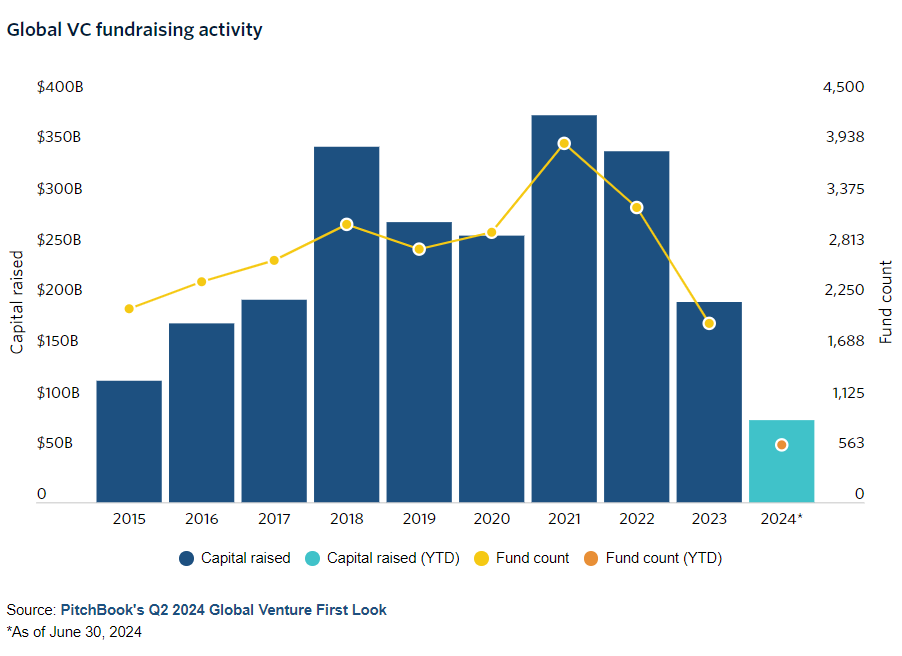

Fundraising for VCs is still not an easy job

Globally, the amount of capital raised is $80.5B, data until June 30, 2024. This represents 41% of the amount raised in 2023, suggesting that the difference between both years will not be that significant.

The average time to close fundraising for US VC funds has increased to 17.2 months, from 15.3 months in 2023

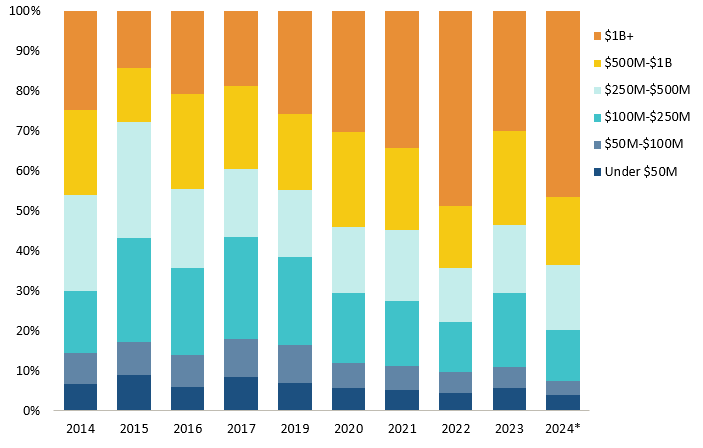

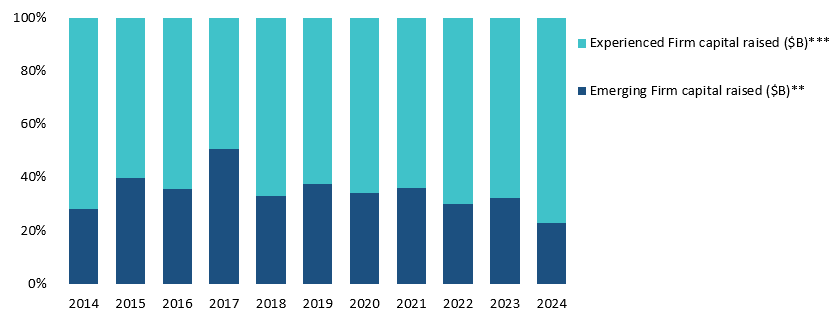

Experienced funds are driving most of the capital raised YTD, mainly because these funds are larger than those from emerging managers. Therefore, even thought the number of experienced funds is similar to that of emerging ones (127 emerging funds vs 128 experienced funds), they raised more than 3 times the amount of capital. - data from US VC funds

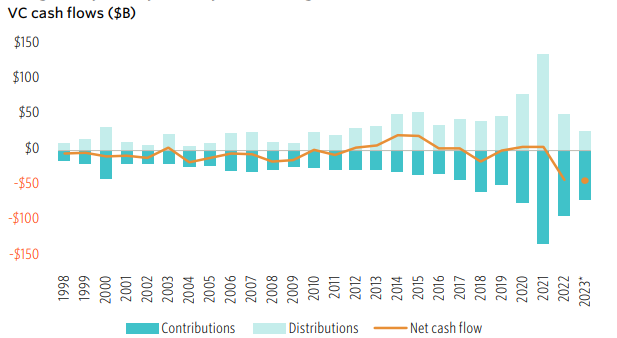

And why does that scenario persist? LPs need liquidity

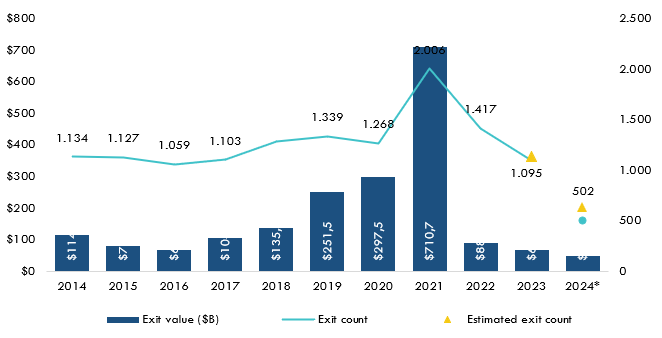

VC has been in the red for 2 consecutive years now (2022 and 2023), this scenario is happening due to a number of reasons, but mainly due to high interest rates and low exit activity. As a result, LPs are not receiving distributions from their VC investments and not making more investments, since there is a limit to the % allocated to the asset class by family offices and institucional investors.

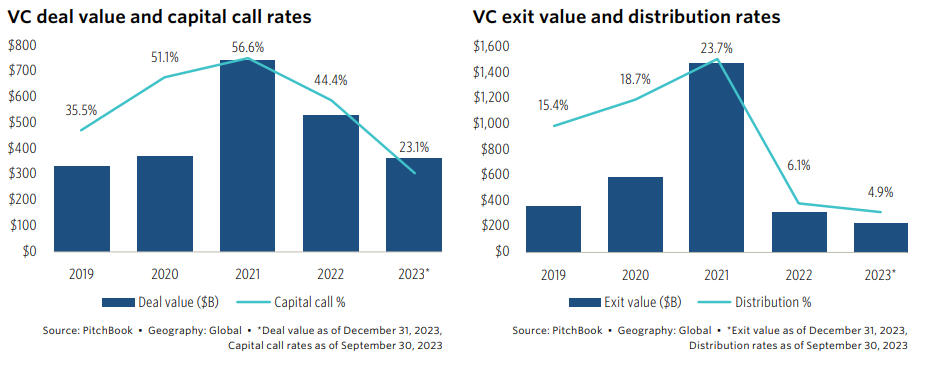

Seeing Figure 5 it’s possible to see exactly what happened during the period displayed. The rise in capital calls in 2021 reflects the excitment around that time and high exit activity, with a significant distribution of NAV (net asset value). In 2023, both metrics are on their lowest points.

The data above is from 2023. However, in Q1 and Q2 of 2024, there were more capital calls compared to the same period last year, according to Carta. Exit activity until July 30th is at 75% the amount seen in 2023, with over 70% of exits occurring through acquisitons. This doesn’t portrait a scenario as bad as 2023, but not much better.

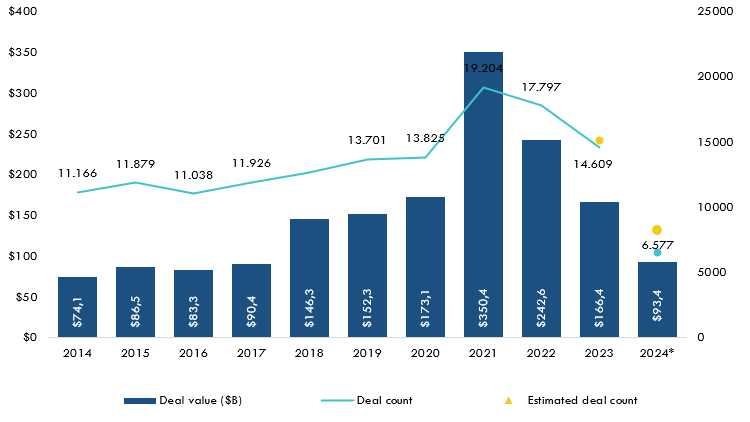

VCs are more diligent with investments, however deal activity is growing, surpassing 55% of last year’s raised amount as of June

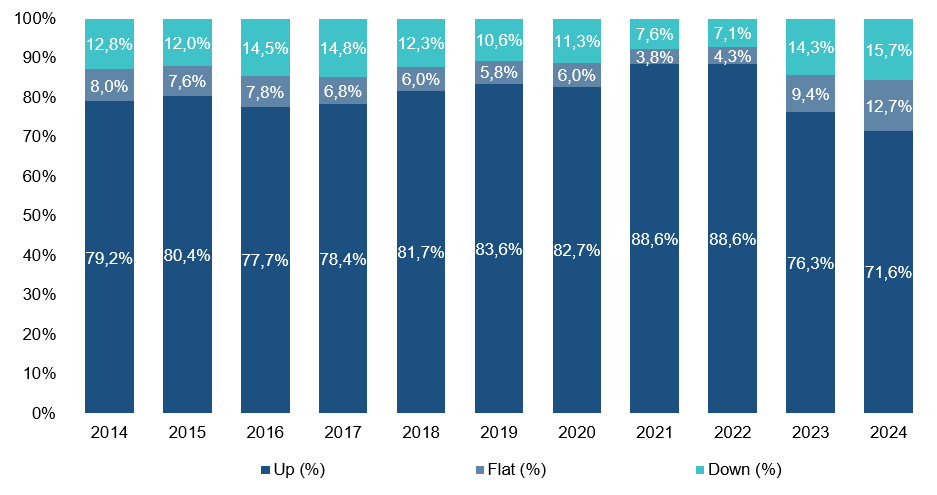

Most of the deals in 2024, up to June, are early-stage and pre-seed/seed. However, there is already a higher percentage of venture growth deals, compared to 2023, probably due to the mega rounds for AI startups. The scenario this year seems to be continuing the trend of down and flat rounds, increasing slightly the % of those funding rounds when compared to last year (despite 2024 data being only until june).

71,6% of funding rounds were up rounds, compared to 76,3% in 2023

12,7% were flat rounds, compared to 9,4% in 2023

15,7% of down rounds, compared to 14,3% in 2023

As of June 30th, 2024, there were 138 unicorn deals in the US, where AI startups had a 42% share of those. Looking at all fundraising activity 41%, in deal value, came from the AI & ML sector and in Q2 2024, almost have of all deal value came from this sector (49% to be exact).

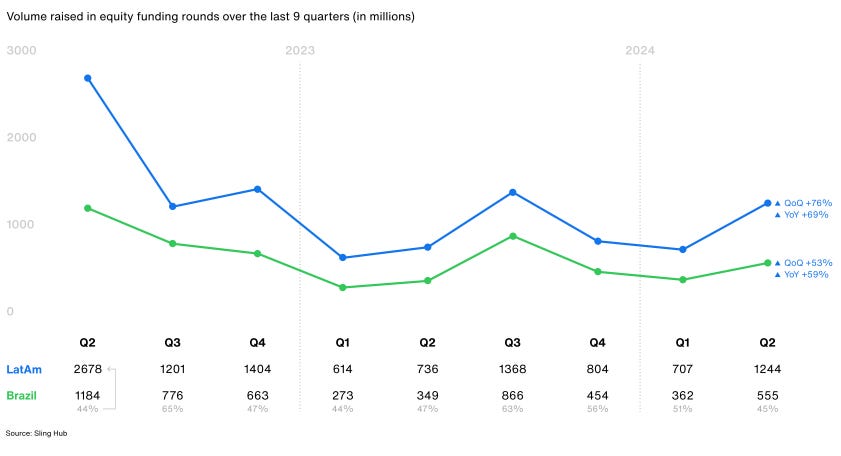

What about Brazil and LatAm?

Equity investment volume in LatAm and Brazil in Q1 and Q2 2024 has been higher than during the same period in 2023. However, the number of funding rounds is lower, indicating that larger rounds are taking place compared to last year.

There were 10 Series B+ rounds in the first half of 2024 compared 16 rounds in LatAm

The region shows similar behaviour as the US data above, being a great reflection of that market.

I think the LinkedIn post below says a lot about the moment today and what’s to come, the unpredictability today is high, with elections in the US, doubts about the effectiveness of AI and its business model and interest rate behaviour. The speech remains the same as the previous year, however there are new pieces in the puzzle that can affect the outcome, especially the overestimation of technology in the short term and underestimation in the long term.

If you have not subscribed yet, subscribe now!

Recommendations

⬛ This one important fact about current AI explains almost everything - Gary Marcus

⬛ The AI Supply Chain Tug of War - Sequoia