How much is enough

Is there a perfect portfolio construction strategy? How VCs choose one or the other? #45

Welcome to another edition of Notes by Letícia, for those that are new here (40+ in the last few days), thanks for subscribing! You can expect biweekly editions all about the Venture Capital market, all based on the topics I've been reflecting on the most. If you're not subscribed yet, subscribe to this newsletter and receive each article directly in your email inbox.

Venture Capital is an asset class where there are several different strategies to achieve similar results. Today, I decided to bring up the topic of different portfolio construction strategies, specifically to understand if there is a perfect portfolio size and how it affects returns.

Each VC fund has its own investment thesis and portfolio strategy, which are built upon previous experiences, sectors and models of interest, market analysis, among several other factors. By focusing on portfolio construction strategy, I see that it's possible to break down this construction into a few decision points:

Number of new investments

Amount reserved for follow-ons

Average investment ticket size

Level of support for each startup

and many others

Like I said before, we see different strategies to achieve similar results, which is to bring the highest possible return to your investors. However, if we analyze some studies on the subject, we can see a common thread, that being: a larger portfolio brings greater certainty of a higher minimum return.

In a research conducted by Moonfire Ventures, a statistical analysis of different portfolios is carried out, differing by the number of investments in each one. I will focus here on three analyses developed by this research, which are conducted by varying the portfolio size.

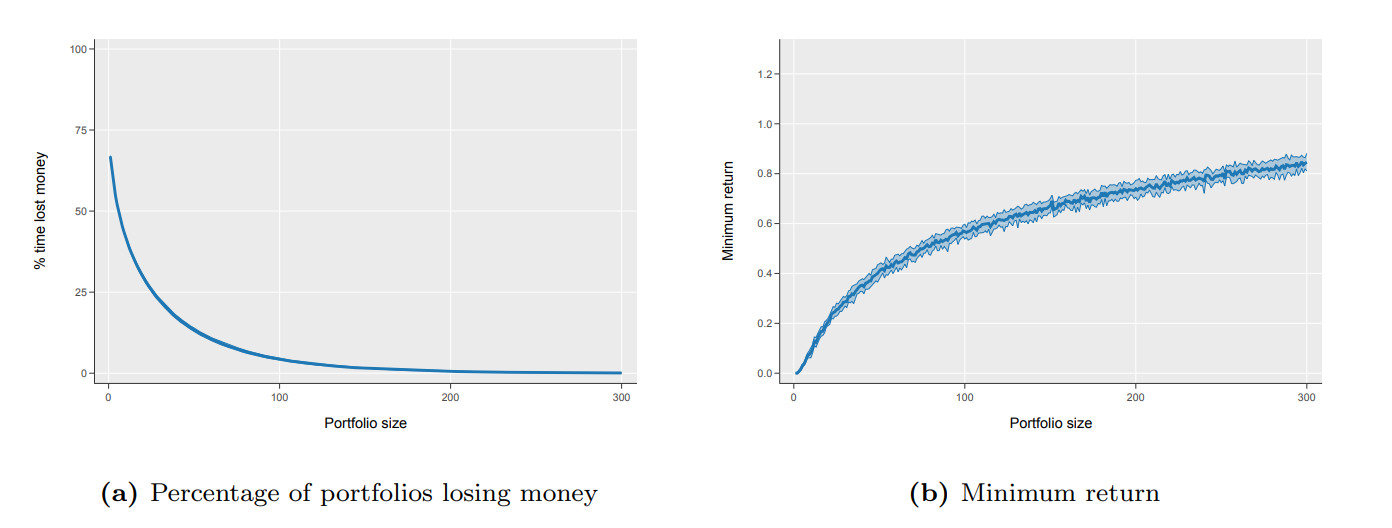

Risk Profile: analysis of the risk of loss and minimum return in each situation

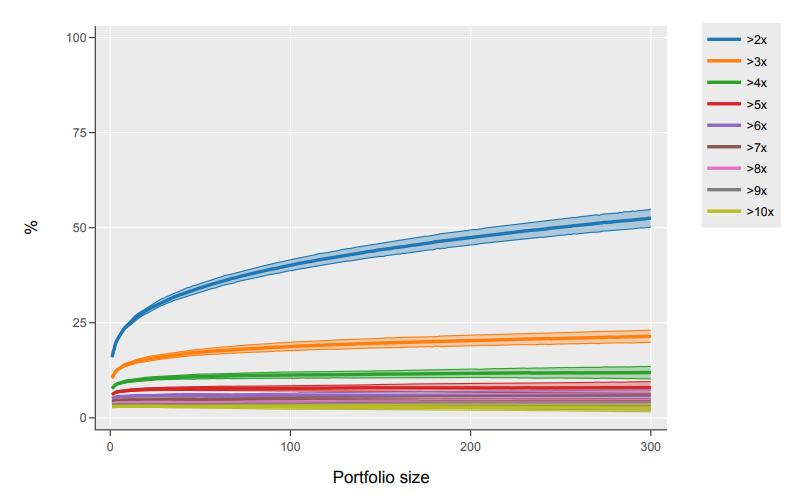

Return Profile: analysis of the frequency at which a certain event occurs

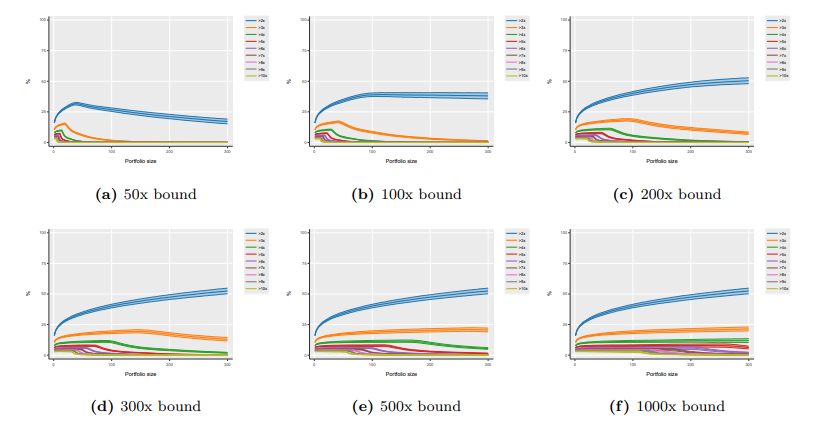

Return profile considering a bounded return on each investment: similar to the previous point, but considering a fixed ceiling for the return on each investment

First, It's important to note the assumptions made to develop this research. It considers a 3 year deployment time, with 60k possibilities of startups to invested in, with these samples drawn from a power law distribution. If you want to know the reasons behind this assumptions I suggest you read the research in full. Now, here are some highlights from the research:

As you increase the portfolio size, the minimum return also inscreases (b). If you have more chances to make a good investment decision (aka great return when the exit happens), it decreases the probability of losing money (a).

When requiring a 2x - 5x return, larger portfolios make a difference on the probability of that actually happening. However, for returns 6x or higher, the portfolio size doesn’t seem to change the probability of that happening.

The return on each investment is limiteless, however, historically it is not exactly that. Considering different scenarios where each investment has a specific return cap, the smaller the cap, the smaller portfolios appear to have a higher probability of achieving a higher return.

Thinking about it, the results above make a lot of sense.

Investing in more startups gives me a greater chance of finding those that will return the fund. Therefore, there is a lower chance of losing money and a higher minimum return is observed - Figure 1

However, the winning returns need to offset the losses, and the greater the losses, the more significant returns I need to have. That said, when aiming for higher returns, a large portfolio is not necessarily needed to achieve that, in fact, it dilutes the positive results. - Figure 2

Especially when ROI is bounded. In this case, the lower the bound, the smaller the portfolio size needed to achieve significant returns (6x +). This makes sense, given that by increasing the return threshold for each investment, there is more opportunity to offset losses (large portfolio) and still bring in a good return. - Figure 3

Now, let’s bring this theory into the real world. In a Rebel Fund article, it is shown that if you had invested in all YC startups at Demoday, since 2005, you would have achieved 176% average annual return net of dilution. However, this is something almost impossible to achieve (expect for YC itself), for different reasons, one of them being the intense competition in some of the investment rounds. If possible, this case would be a great example to see the study in practice, with a large selection of startups receiving the same amount of investment. The detail in this case is that this group of startups has extremely high quality.

And smaller, more concetrated portfolios? Where do they fit in?

This strategy necessarily implies that you trust in your ability to make the best choice. That is, with a smaller number of 'chances', there is less room for error.

Additionally, I see that there are other important points behind the decision to pursue this strategy:

High level of support and attention to the portfolio: reduces the risk associated with the investment

Round terms and limited fund size: limits the number of possible investments to be made

Differentiated returns: according to the study, the higher the targeted return, the greater the probability of it happening when the portfolio is smaller

Level of access: building market reputation, having better access also tends to reduce risk.

As you can see, there doesn't seem to be a right or wrong decision when talking about portfolio construction. What matters at the end of the day is understanding why each decision is made and its influence on returns for their limited partners.

If you’ve read this far, share this newsletter with your network!

Here are some contents that inspired this edition:

How Portfolio Size Affects Early-Stage Venture Returns - AngelList

972 billion portfolios: How to design the optimal venture portfolio

Recommendations

⬛ AI startups: Sell work, not software

⬛ Capex & Opex supercycle - the dusk of SaaS and the dawn of AI-SaaS

Excelente👏🏼