The gap between costs and revenue in AI, Brazil's Travel Tech sector and other thoughts

The gap between costs and revenue in AI, Brazil's Travel Tech sector and other thoughts

Highlighting great articles I read lately #51

Welcome to Notes by Letícia, a biweekly newsletter, about my perspectives and thoughts about the Venture Capital market. The objective is to bring a new discussion/topic, based on what I’m reading, market data, or just some thoughts on the market in each new article.

If you are interested about this market, subscribe to this newsletter, and help us get to more people!

This week's newsletter edition is full of different topics, but before starting, I would like to share here the latest article, in collaboration with the I'm no Economist newsletter, where I talked more about that different business models can obtain the highest returns.

Now, let's move on to today's edition:

Highlights of articles I've read recently

Study from Onfly about the state of Brazil’s travel tech sector

Incentives can vary for each stakeholder in an exit opportunity

I have been commenting on this topic for some time now (here and here), the difference in incentives and needs of different stakeholders within the Venture Capital business model. In this article by David Beisel, VC at Next View, he writes about an experience of divergence between different investors and founders at the moment of an exit opportunity. This arises from different expected scenarios that are relevant to each type of investor within the same cap table, as well as the need for returns for investors depending on the timing of the fund.

This situation is inevitable given the increase in the size of VC funds, therefore founders and investors need to choose carefully to ensure alignement between all stakeholders. Investors also need to be diligent when analyzing opportunities to understand the expected exit time for the company and the amount needed to get there, to avoid being caught in a situation where it does not make sense for new investments.

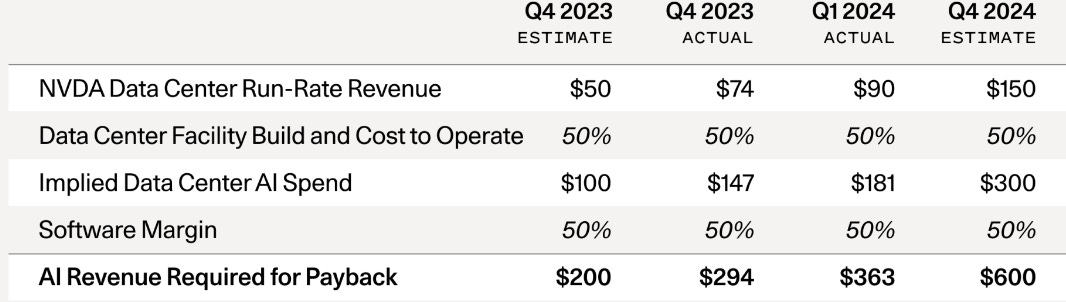

The gap between costs vs revenue in AI today

Recently, an article from Sequoia provided an approximate calculation of the current gap between costs and revenues for companies that are investing heavily in AI, such as Google, Microsoft, and Meta. The result is quite significant, even given the high revenue of these companies, $600 billion, primarily due to the cost of GPUs, maintenance, and the margin needed to operate.

This scenario primarily arises from the race to build computational power and the fact that the value delivered to customers is not yet reflected in increased revenue. That is, customers are not yet seeing the promised increase in efficiency from AI models to the extent that they are willing to pay more for it and/or increase their investment in the technology.

In this scenario, NVIDIA and OpenAI have been the main beneficiaries, with over 400% year-over-year revenue growth in their data center lines and over $3 billion in ARR, respectively. This leadership is due to several factors, but two significant ones are: (i) first-mover advantage and (ii) scaling factors for neural models, which include model size, data, and compute. In this framework, NVIDIA leads in compute, and OpenAI leads in models.

The current moment reflects the beginning of a platform shift, with significant investments, many of which do not yield short-term returns but rather help to build the infrastructure for the development of future solutions. Therefore, I believe there is still much to happen in the next years.

If you want to read more on the topic, I recommend the following articles:

State of Brazil’s travel tech sector

As I have mentioned here a few times, here, for example, there are some markets which still have a lot of room for exploration, however not many people are taking advantage of it. This is also the case in the travel tech market, but with a significant point: the market is still largely made up of small companies. In other words, according to the research conducted by Onfly on the travel tech market in Brazil, it is shown that most of the mapped companies have fewer than 10 employees, 35.6% to be exact. However, even so, there are major success stories in the sector, such as Buser, which raised R$ 700 million in 2021, with a long history of fundraising since 2018, swith a seed round.

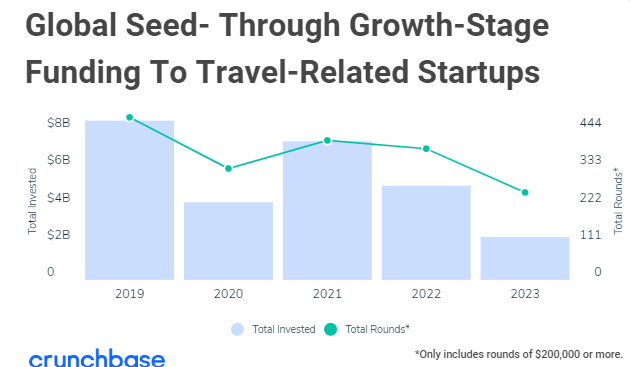

When looking globally, the investment landscape presents the following volume:

The decline observed in 2022 and 2023 cannot be analyzed separately from the current context of lower investments across all sectors compared to previous years. One might wonder whether the pandemic's effects are still impacting current investments. There are indications that the market has returned to its pre-pandemic state. According to ONU Tourism, it is estimated that 2024 will reach the same level of revenue as before the pandemic in the tourism sector. Moreover, according to the Global Business Travel Association, most professionals believe that 2024 will be the year of near-total recovery for the sector.

Given this scenario, I see that there are opportunities to unlock value in this market, such as:

Connecting ends: Omnibees is an excellent case, working on connecting and managing different sales channels to increase conversion.

Digitization of something informal/that has a poor experience: Buser case fits exactly here, where the solution offers a new experience for the user, being 10 times better than the previous experience

Digitization of processes: digitalizing processes that are repetitive and can be executed in a more efficient way, managing corporate expenses and travel, for example

AI as a concierge: making the experience of planning, scheduling and travelling more time efficient and personalized, with tools such as, concierge and travel planning apps.

And, when talking with Vinicius, CMO at Onfly he shared his views on the market as well:

Connecting the dots of the journey will be the main challenge of the new decade.

Since 2018, AI has attracted about two-thirds of all technology investments in the travel and mobility market, showing that it is here to stay. Despite this, companies in the travel market still face significant challenges in interconnecting their tools and technologies, with little connectivity between APIs.

This lack of integration results in data loss for decision-making and hinders the traveler's experience, who has to make phone calls to reschedule flights or wait while the hotel receptionist looks up their reservation in several different systems.

The main area of investment for travel tech companies in the coming years will be focused on streamlining internal and back-office processes among existing technologies to increase the efficiency of their value chains. - Vinícius Ribeiro, CMO at Onfly

If you want to dive deeper into the study conducted by the Onfly team in more detail, click here. And if you’re building something on this sector, let’s talk!

Recommendations

⬛ Seeing Like a Network - Rohit Krishnan

⬛ AI Apps Deliver Outcomes - So Why Are They Still Charging Like Old School SaaS? - Julia Maltby