Aligning Founder and VC Expectations on Valuation and Market Size

And why it is important for a VC #50

Welcome to Notes by Letícia, a biweekly newsletter, about my perspectives and thoughts about the Venture Capital market. The objective is to bring new discussions, based on what I’m reading, market data, or just some thoughts on the market in each new article.

If you are interested about this market, subscribe to the newsletter, so that you receive it directly in your email! This is the 50th edition of Notes by Letícia, and it is only the beggining!

I believe everyone has already heard phrases like “USD 1 billion in valuation is not enough,” whether in meetings, videos, or posts on LinkedIn. As I have written before (here), Venture Capital is a game of extremes, and this is another case where it is no different.

Today, I aim to bring a bit more rationale behind this phrase and understand why it does or does not make sense.

Knowing this, let's explore two topics:

What valuation does a startup need to achieve to be considered a fund returner for the VC (a successful investment)?

What is the minimum market size for the investment to make sense for a VC?

In an ideal world within a VC fund, most startups would bring the majority of the returns, all would be fund returners (returning a multiple of the total fund value), and there would be no risk. But that’s not how the world works. In real life, the fund’s return comes from a smaller number of startups.

Since this is how the real world works, at the time of investment, all startups need to have the potential to be the best-performing in the portfolio because at the beginning you don’t really know who will be responsible for the return in the end. This is where the concept of a fund returner comes in. To break even, it is minimally necessary for the investor to return the entire value of the fund (considering there is recycling and the entire value is indeed invested), and the higher the multiple in relation to the size of the fund, the greater the success/performance of that fund.

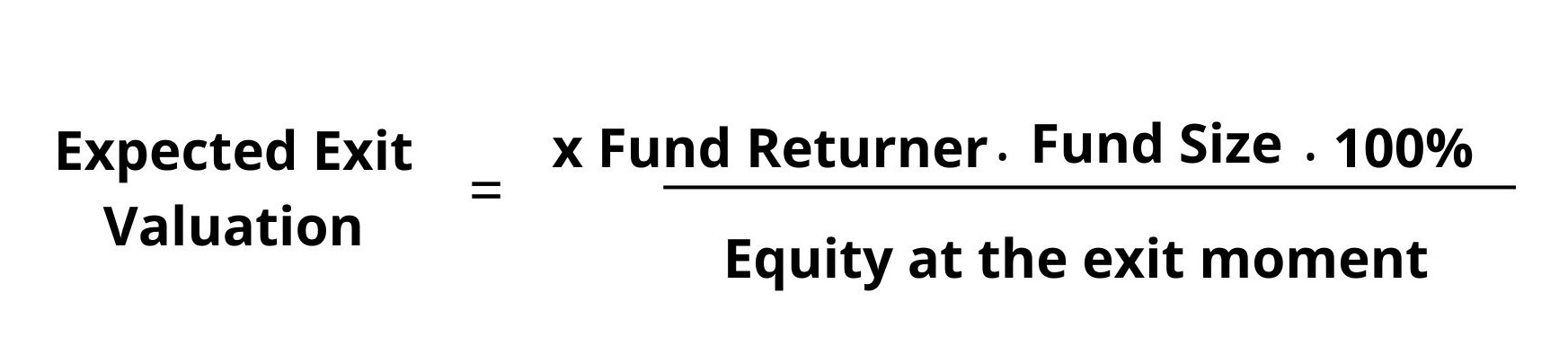

So, let's start with the first question: at the end of the day, what value (valuation) does the startup need to achieve so that, considering the investor's stake, a multiple of the fund size is returned?

To determine this valuation, the following variables are considered:

Multiple of the fund size (x fund size)

Fund size

Equity amount at the time of exit

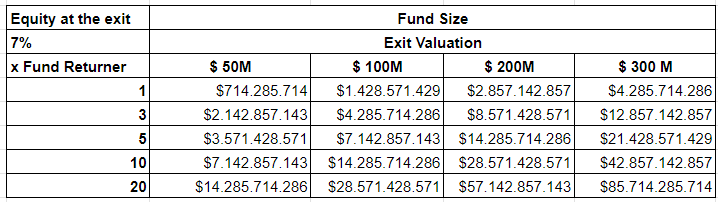

Considering fund sizes from $50M to $300M:

Observing the results, it is possible to conclude a few things:

The larger the fund, the greater the amount needed to return a multiple of the fund.

Valuation is proportional to the fund's perfomance, therefore, the larger the fund, the higher the expected valuation.

The lower the equity at exit, the higher the minimum valuation expected.

The difference in outcomes to achieve the same multiple of the fund is very large, from $2.1bi to $12.8bi, for the same 3x multiple.

It's clear where the differences in incentives and positioning come from. An exit of more than $1bi valuation is necessary for a $100M fund to achieve just a 1x fund size, whereas for a $50M fund, this would be a 2x. It is also important to notice that the situation calculated above only considers the first investment, it doesn’t take into account follow-ons. Therefore, the equity dilution during the investment rounds needs to be taken into account as well, to determine the equity at the exit.

💡Side note: the multiples shown above are different from the multiple obtained considering the entry valuation, because the entry values are not the same. For example:

Let's suppose that:

VC Fund Size: $50M → aiming 3x Fund Returner → Startup Valuation: $2.1bi

Startup Post-Money Valuation in a given investment round: $ 52M

To reach the valuation the fund expects, it is necessary to multiply its valuation by 40x. 💡

Given this, it is important to be clear about what will be necessary to achieve the expected valuation: growth rate, valuation, time, ambition, and market size.

Moving on to the second question of the article, market size is one of the main points of analysis for a VC, simply because a large available space for growth is necessary due to the need for high returns. Now, the question arises: but what is the minimum size that makes sense?

If we consider revenue of over $190M, a range typically seen in companies at the time of IPO, the market size ranges from $6.3 billion to $1.2 billion, for a market share of 3% and 15%, respectively.

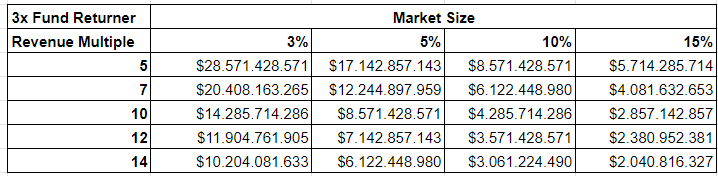

In the same way, it is possible to determine the market size for the cases outlined above, considering a $100 million fund aiming for a return of 3x the fund size:

Observing the calculation above, it is noted that in the best-case scenario, the smallest market size found was approximately $2 billion.

The calculations above help to understand the math behind Venture Capitalists' decisions, but practice is not as precise as reality. When considering market size, some points need to be taken into account:

Preemptive judgment: cases like Airbnb and Uber ended up creating their own markets, and at the time of their early rounds, many investors passed on the deal because they tried to answer this same question and found a number smaller than expected.

Alignment between different funds in the VC journey: when calculating the expected valuation based on fund size, smaller funds will result in a much smaller number than larger funds. However, during the company's growth, both early and late-stage funds are involved, and they have different models, with later-stage funds requiring a higher expected valuation.

As I mentioned, the exercise above is not meant to provide an exact value but to understand how incentives work in this market. The difference in expected return is one of those aspects, in The Puritans of Venture Capital, Kyle Harrison brings a great explanation about that:

There is a dichotomy that exists with capital allocation give-and-take between GPs and LPs. On the one hand, its hard to generate high returns on big pools of capital. GPs can't usually deploy billions of dollars and still generate 5-10x returns. But on the other hand, the same is true for LPs. If you're managing a $100B endowment, its really hard to only deploy $5-10M checks. You'd have to back 1-2K managers if you want to have a $10B venture capital book. But if you can write $250M checks a pop? That's more in the realm of possible. You don't need to generate 5-10x returns on $250M. - The Puritans of Venture Capital

Therefore, when pursuing the venture capital path, it is important to understand the journey you want to follow and to seek investors who are aligned with this outcome.

Here are some articles that inspired this issue:

Exit in Public #8: Diferentes perspectivas sobre a matemática do VC

Big Winners and Bold Concentration: Unveiling the Secret Portfolio Returns of Leading Venture Funds - Jason Shuman

Recommendations

⬛ State-Space Models Are Shifting Gears - Sivesh Sukumar (Investor at Balderton Capital)

⬛ The Hardening Of The Great Softening - Investing 101

⬛ Real-time payments in 1,000 words - Matt Brown's Notes

Well written and insightful! Congrats!